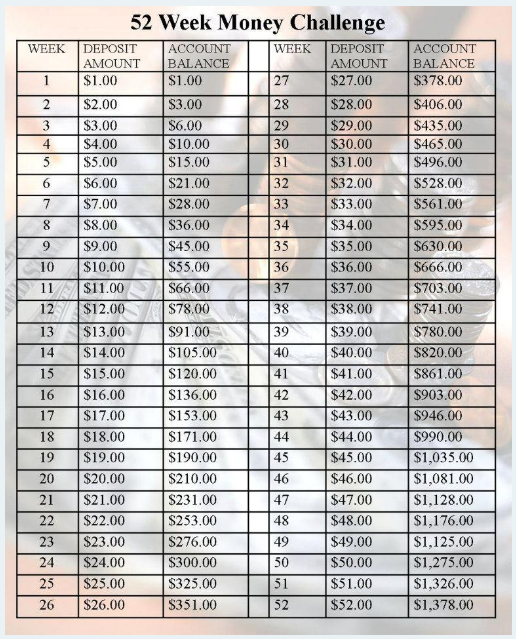

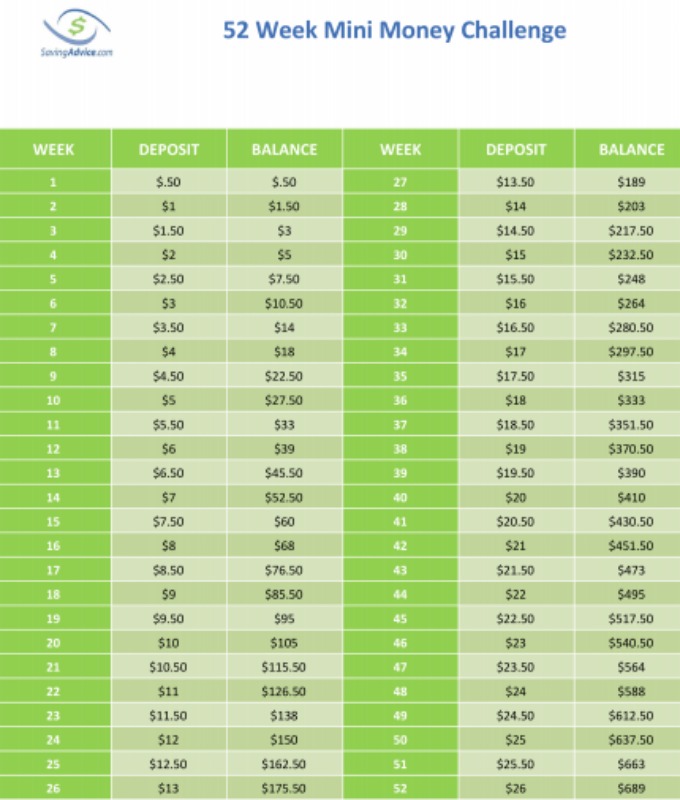

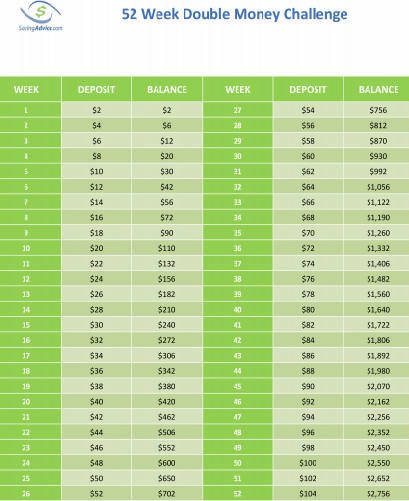

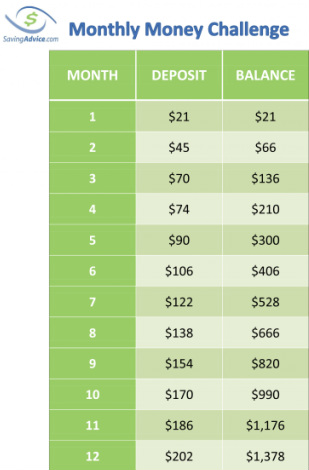

Let's get serious it is 2014 where our economy is as flimsy as a a piece of paper who knows if we will be able to enjoy our retirement when we get older. Saving money is something that we all need to look at in a more serious manner. I mean with the average college student graduating in this day of age has a an average of $27,000 in debt in student loans just from undergrad alone. With this statistic being the poster child for our generation we have to be more responsible and be prepared when it comes to our finances. Saving money is a enjoyable experience just the thought of checking your savings account to see almost $2,000 just sitting waiting for you can be a exhilarating. If you follow some of the 52 Week Money Challenges I have posted below you could make my last sentence a reality. Saving money now is going to be a necessity for our livelihood in our future . In this blog post I will feature different articles geared towards financial advice for young adults like ourselves from Forbes and CNN. So check them out and educate yourself if you haven't already about your finical future.

| Be tight-fisted with your dollars. A single dollar can have incredible value. When was the last time you got fast food at the drive-thru? It may have been convenient, but it certainly wasn’t inexpensive. When you add grabbing coffee in the morning, a smoothie, fast food and a candy bar when you’re filling up your gas tank, these seemingly insignificant items can easily add up to $20 a day, $100 a week and $400 a month. That’s a car payment. Obtain and keep a good credit score. A strong credit score can make all the difference between securing the apartment you want and losing out in a competitive rental market. In our case, we missed the boat on helping our kids establish credit early. |

| Keep your overhead low. Subscription model pricing can help consumers keep upfront costs down. This can be a good thing as long as it doesn’t get out of hand. Sure, it’s nice to listen to Pandora without commercials and it seems like a bargain at $3.99 a month. But would you really shell out $48 if you had to hand over cash from your wallet just to have commercial-free internet radio for the year? Consider this line of thinking with all recurring expenses we have today: cable TV, cell phones with data packages, satellite radio and internet. For entertainment we have Netflix, Hulu, and Amazon Prime. These “necessities” can easily run upwards of $250 a month if you aren’t careful. Cut the ones that aren’t truly “needs” to keep your overhead low. |

|

| Sock money away. Saving money by skipping a latte or bundling your cable and internet is one thing, but putting that savings in the bank and keeping your hands off it is another. Socking away money that you don’t touch is paramount to success. There are a couple of ways to ensure that this happens: You can set up an auto-draft from checking to savings, open a savings account at a different bank so you can’t easily transfer funds between accounts, or skip the debit card for your “don’t-touch” savings account. Do whatever it takes to make the savings stick. Unfortunately, most Americans live on the edge when it comes to money. According to recent research by Bankrate.com, 76% of Americans are living paycheck to paycheck, and a study from CashNetUSA reported that 46% of people surveyed had less than $800 saved for emergencies. This lack of financial stability makes us all vulnerable. When an emergency hits and we get a call from a family member for help with a rent deposit or moving expenses, are we going to turn them away? Of course not. We are going to help, but those funds have to come from somewhere. When 20-year-olds can manage their cash, are able to borrow money at decent rates and live on 75% of their income by doing the above, that means financial security not just for them, but for the entire family. |

| Switch to frugal mode. The ability to kick into “super-saver mode” for a stint is vital when unexpected expenses come up or income suddenly drops. This could involve skipping taxis and taking public transportation, bringing PB&J sandwiches to work, stretching hair care products, switching to basic cable and “go phones,” getting a roommate, ride sharing, going to free concerts, and skipping restaurants to have friends over instead (with a dish in hand)—whatever it takes to make ends meet. Frugal mode helps you avoid resorting to credit cards in a crunch. Begin retirement planning with your first job. This tip is so important. If the company you work for offers a 401(k) plan, sign up at your first opportunity. If there's no such plan, divert some of your paycheck into an IRA. Believe it or not, if you're lucky, one day you'll find you are older, so it's best to be prepared. Setting up automatic contributions to either one of these retirement vehicles at a young age will help you build wealth painlessly. Just as an example, let's say you invest $200 a month beginning at age 25, and you earn 7 percent annually on that money. By the time you turn 65, you will have about $525,000 saved up. If you wait until you're 35 to begin saving, assuming the same monthly investment and rate of return, you'll have amassed less than half that amount -- about $244,000. This illustration simply shows the impact that a 10-year head start can make on your savings, thanks to the magic of compounding. Do the math yourself with Bankrate's retirement calculator. |

|

Read more: http://www.bankrate.com/finance/retirement/10-financial-tips-for-young-people-1.aspx#ixzz2tFhxalhg

Follow us: @Bankrate on Twitter | Bankrate on Facebook

7 Financial Skills Every 20-Year-Old Needs To Learn By: Nancy Anderson, Contributor

Follow us: @Bankrate on Twitter | Bankrate on Facebook

7 Financial Skills Every 20-Year-Old Needs To Learn By: Nancy Anderson, Contributor

RSS Feed

RSS Feed